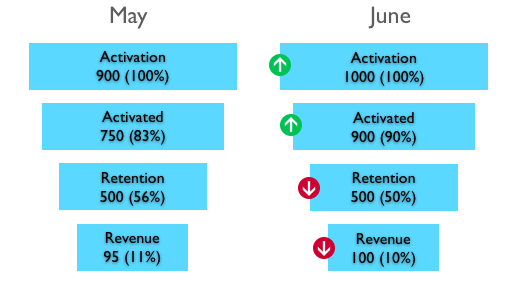

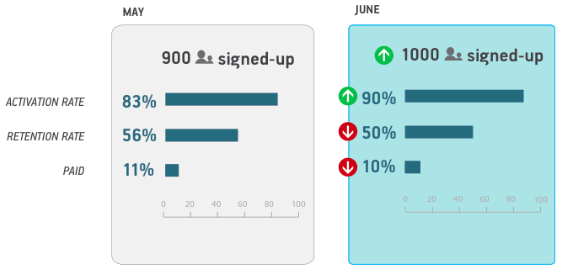

It’s that time of the year again: Gartner has released its report on Business Intelligence and Analytics platforms. One year ago we looked at how the data in the Magic Quadrant – the two-dimensional space of execution vs. vision – can be used to visualize movement over time. In fact, the article Gartner’s Magic Quadrant for Business Intelligence became the most viewed post on this Blog.

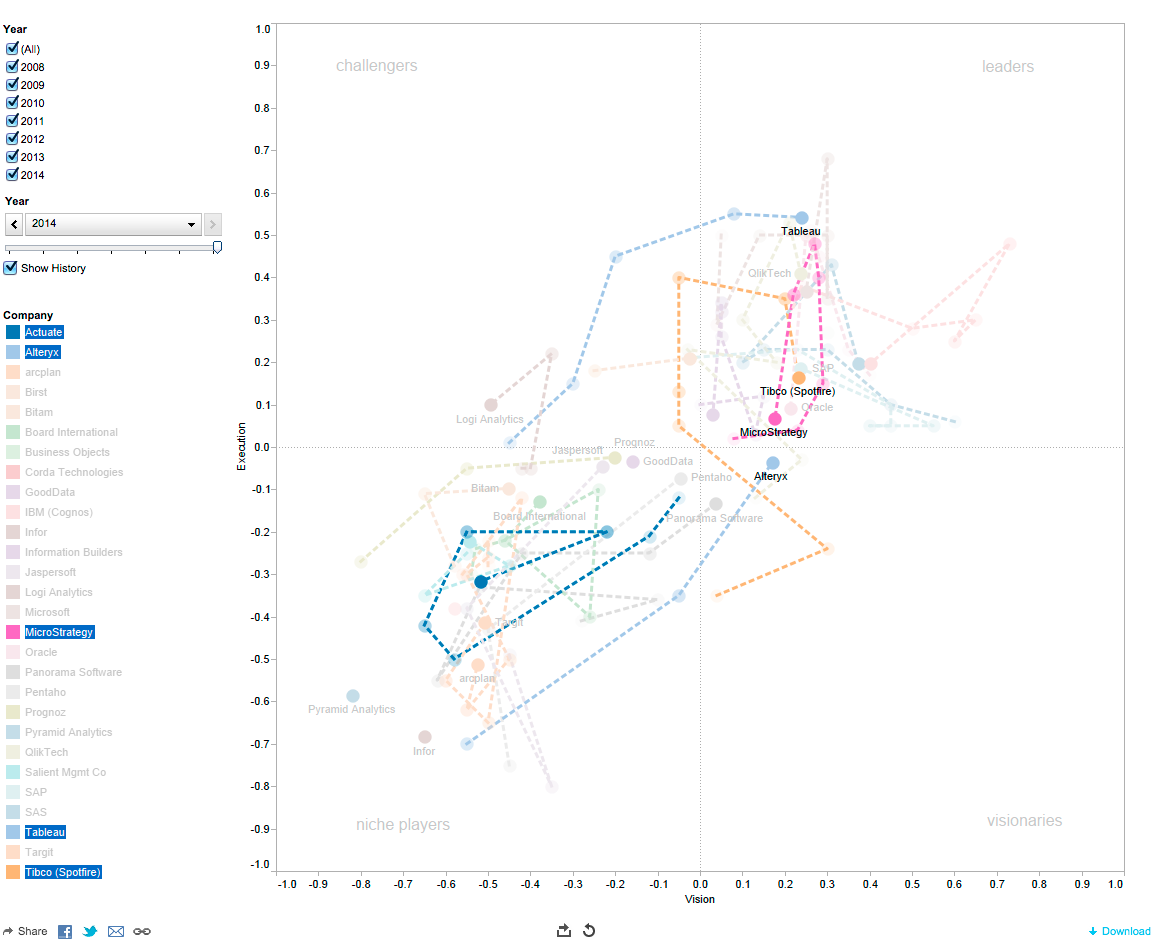

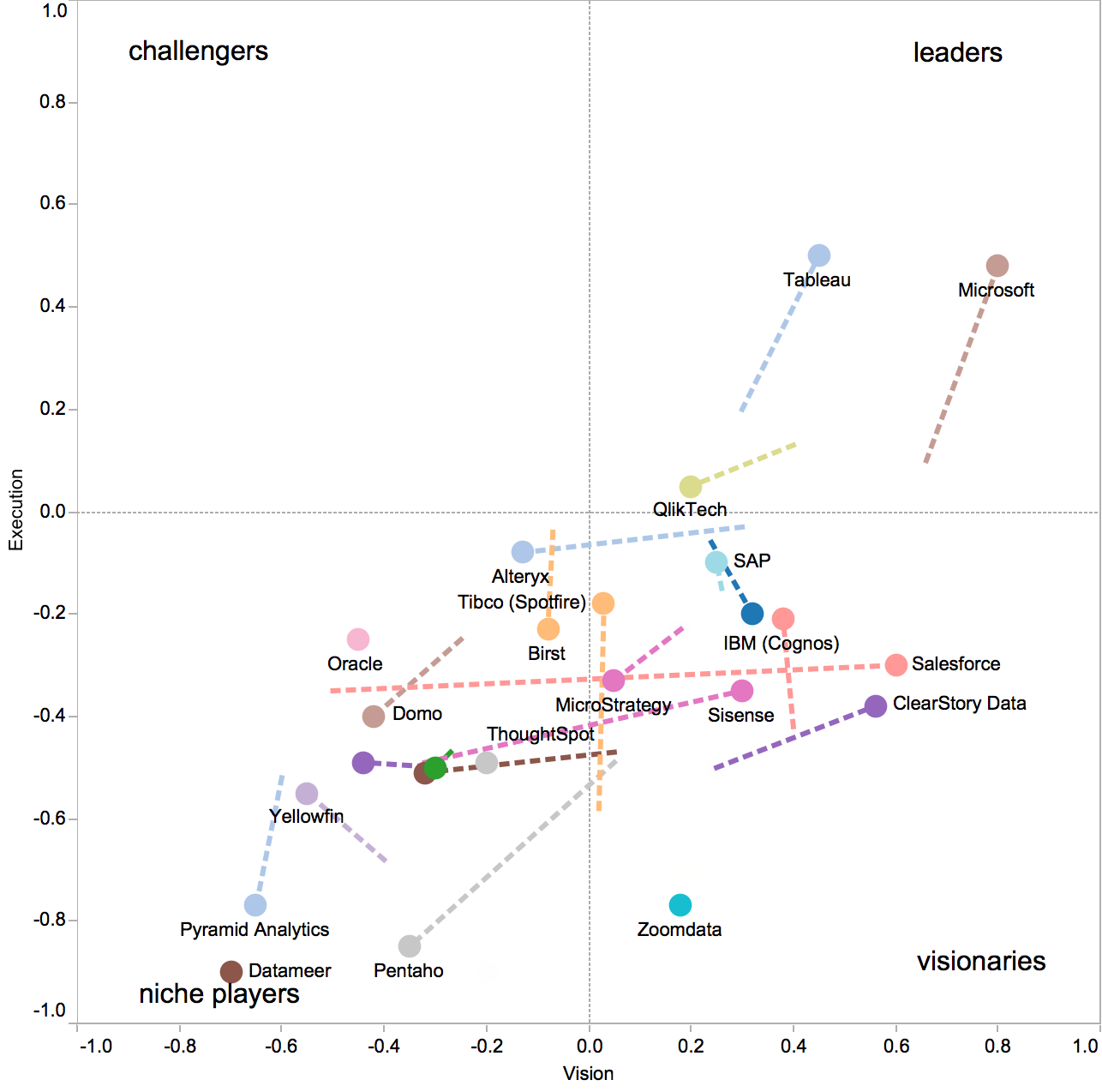

I had also uploaded a Tableau visualization to Tableau Public, where everyone can interact with the trajectory visualization and download the workbook and the underlying data to do further analysis. This year I wanted to not only add the 2013 data, but also provide a more powerful way of analyzing the dynamic changes, such as filtering the data. For example, consider the moves from 2012 to 2013 of some 21 vendors:

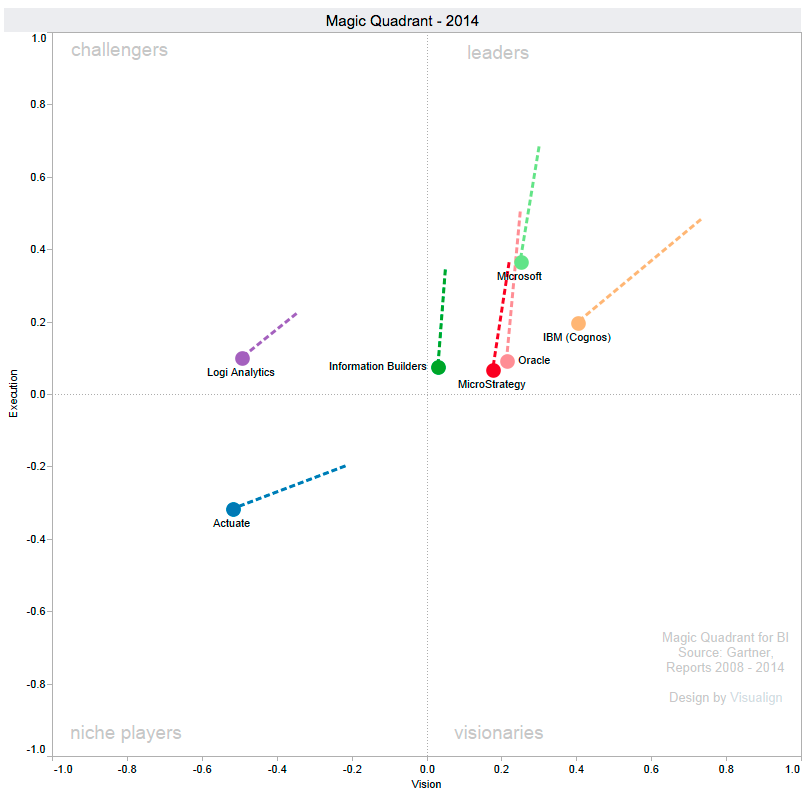

Gartner’s Magic Quadrant for Business intelligence, changes from 2012 to 2013

It might be helpful to filter the vendors in this diagram, for example to show just niche players, or just those who improved in both vision and execution scores. To that end, I created a simple Tableau dashboard with four filters: A range of values for the scores of both vision and execution scores, as well as a range of values for the changes in both scores. The underlying data is also displayed for reference, which can then be used to sort companies by ordering along those values.

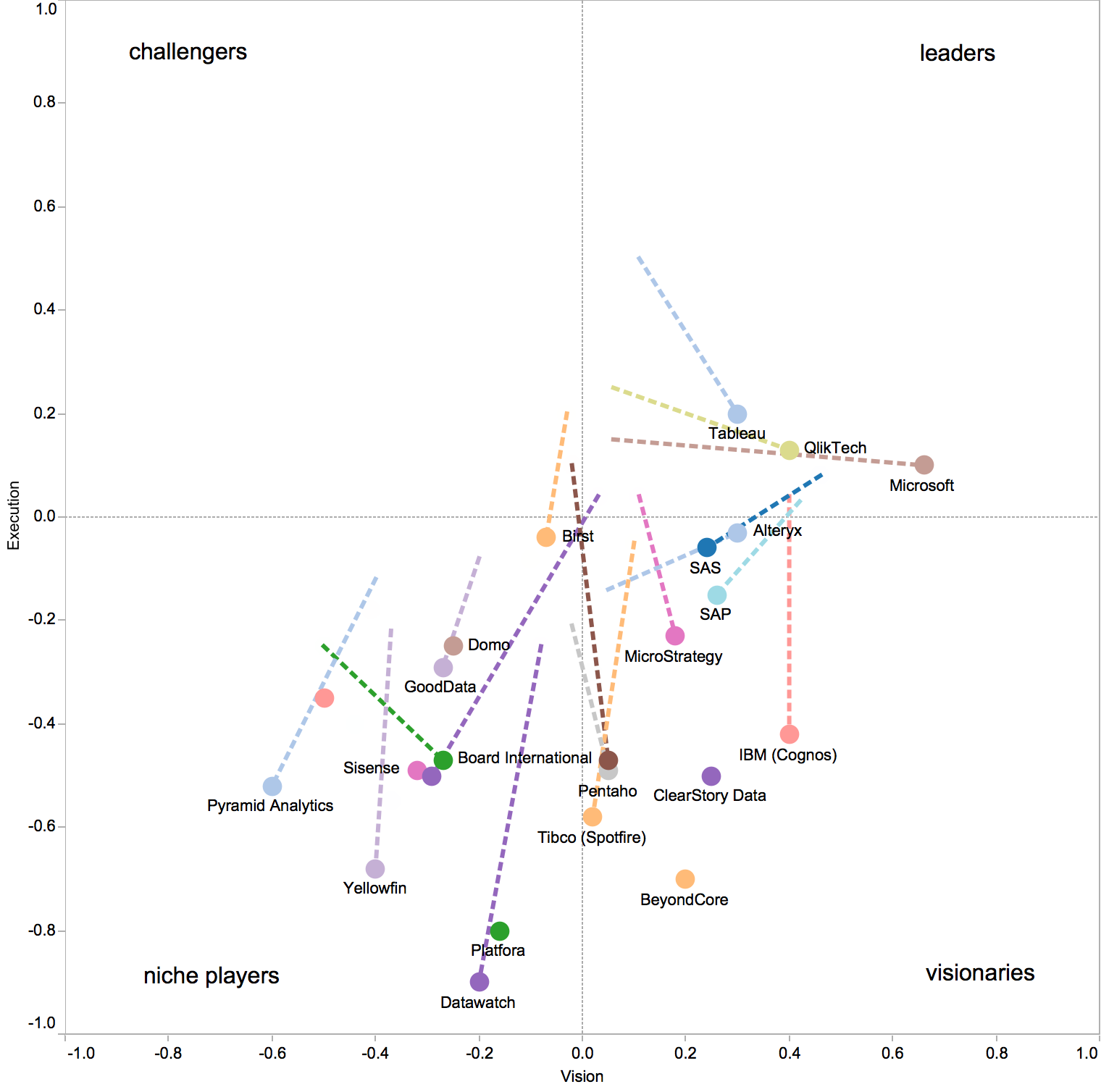

Here is an example of the dashboard set to display the subset of 15 companies who increased either both or at least one of their vision or execution scores without lowering the other one.

Subset of companies who improved vision and/or execution over the last year.

That’s more than 70% of platforms, with the increase in vision being more pronounced than that of execution. That’s considerably more than in the previous years (2013: 15; 2012: 6; 2011: 6; 2010: 3; 2009: 9) – making this collective move to the top-right perhaps a theme of this year’s report.

Who changed Quadrants? Who moved in which dimension?

Last year Tibco (Spotfire) and Tableau were the only two platforms changing quadrants, then becoming challengers. This year both of them “turned right” in their trajectory and crossed over into the leaders quadrant due to strong increases in their vision capabilities. (QlikTech had been on a similar trajectory, but already crossed into the leader quadrant in 2012. It also strengthened both execution and vision again this year.)

Another new challenger is LogiXML. Thanks to ease of use, enhancements from customer feedback and a focus on the OEM market its ability to execute increased substantially. From the Gartner report summary on LogiXML:

Ease of use goes hand-in-hand with cost as a key strength for LogiXML, which is reflected by its customers rating it above average in the survey. The company includes interfaces for business users and IT developers to create reports and dashboards. However, its IT-oriented, rapid development environment seems to be most compelling for its customers. The environment features extensive prebuilt elements for creating content with minimal coding, while its components and engine are highly embeddable, making LogiXML a strong choice for OEMs.

A few other niche players almost broke into new quadrants, including Alteryx (which had the biggest overall increase and almost broke into the visionary quadrant), as well as Actuate and Panorama Software.

The latter two stayed the same with regards to execution (as did SAP) – while all three of them moved strongly to the right to improve on the vision score (forming the Top 3 of vision improvement).

Information Builders and Oracle stayed where they were, changing neither their execution nor vision scores.

Microsoft and Pentaho stayed about the same on vision, but increased substantially in their execution scores. This propelled Microsoft to the top of the heap on the execution score, while it moved Pentaho from near the bottom of the heap to at least a more viable niche player position. Microsoft’s integration of BI capabilities in Excel, SQL Server and SharePoint as well as leveraging of cloud services and attractive price points make it a strong contender especially in the SMB space. Improvements of its ubiquitous Excel platform give it a unique position in the BI market. From the Gartner report:

Nowhere will Microsoft’s packaging strategy likely have a greater impact on the BI market than as a result of its recent and planned enhancements to Excel. Finally, with Office 2013, Excel is no longer the former 1997, 64K row-limited, tab-limited spreadsheet. It finally begins to deliver on Microsoft’s long-awaited strategic road map and vision to make Excel not only the most widely deployed BI tool, but also the most functional business-user-oriented BI capability for reporting, dashboards and visual-based data discovery analysis. Over the next year, Microsoft plans to introduce a number of high-value and competitive enhancements to Excel, including geospatial and 3D analysis, and self-service ETL with search across internal and external data sources.

The report then goes on to praise Microsoft for further enhancements (queries across relational and Hadoop data sources) that contribute to its strong product vision score and “positive movement in overall vision position”. This does not seem consistent with the presented Magic Quadrant, where Microsoft only moved to the top (execution), not to the right (vision). Perhaps another reason for Gartner to publish the underlying coordinate data and finally adopt this line of visualization with trajectories.

Dashboard with filters revealing two platforms deteriorating in both vision and execution

Only two vendors saw their scores deteriorate in both dimensions: MicroStrategy gave up some ranks, but remains in the leader quadrant. The report cites a steep sales decline in 3Q12 and the increased importance of predictive and prescriptive analytics in this years evaluation among the reasons:

MicroStrategy has the lowest usage of predictive analytics of all vendors in the Magic Quadrant. A reason for this behavior might be the user interface that is overfocused on report design conventions and lacks proper data mining workbench capabilities, such as analysis flow design, thus failing to appeal to power users. To address this matter, MicroStrategy should deliver a new high-end user interface for advanced users, or consumerize the analytic capabilities for mainstream usage by embedding them in Visual Insight.

The other vendor moving to the bottom-left is arcplan, which is now at the bottom of the heap in the niche players quadrant.

Who moved to the top-left?

With the dashboard at hand, you can also go back and do similar queries not just for the current year 2013, but any of the five previous years. For example, who has moved to the top-left – improved execution at the expense of reduced vision – over the years?

In 2013 those were Targit, Jaspersoft, Board International. All three of them had a sharp drop in Execution in the previous year 2012. A plausible scenario of what happened is that these companies lost their focus on execution, dropped the scores and in an attempt to turn-around focused on executing well with a smaller set of features (hence lower vision).

In 2012 the only vendor to display a move to the top-left was QlikTech. They had some sales issues the prior year as well, although their trajectory in 2011 was only modestly lower in execution, mostly towards higher vision.

In 2011 Actuate and Information Builders moved to the top-left. Both had trajectories to the bottom-left the prior year (2010), with especially Actuate losing a lot of ground. With the Year slider on the top-left of the dashboard one can then play out the trajectory while the company filters remain, thus showing only the filtered subset and their history. Actuate completed a remarkable turn-around since then and is now positioned back roughly where it was back in 2010.

Dashboard with analysis of top-left moving companies.

(Click on the image above or here to go to the interactive Public Tableau website.)

In 2010 there were five vendor moving to the top-left: Oracle, SAS, QlikTech, Tibco (Spotfire) and Panorama Software. Although in that case none of them did show a decrease in execution the previous year. That focus on execution may simply have been the result of the economic downturn in 2009.

Such exploratory analysis is hard to conceive without proper interactive data visualization. Given the focus of all the vendors it covers in this report, it seems somewhat anachronistic that Gartner in its report does not leverage the capabilities of such interactive visualization itself. In the previous post on Global Risks we have seen how much value that can add to such thorough analysis. (Much of this dashboard should be applicable for risk analysis as well, just that the two-dimensional space changes from platform vision vs. execution to risk likelihood vs. impact!) If Gartner does not want to drop on its own execution and vision scores, they better adopt such visualization. It’s time.

From the entire trajectory (left) one can see that all of them have been leaders for many years.

From the entire trajectory (left) one can see that all of them have been leaders for many years.